Here we are providing Class 12 Accountancy Important Extra Questions and Answers Chapter 6 Accounting for Share Capital. Accountancy Class 12 Important Questions and Answers are the best resource for students which helps in class 12 board exams.

Class 12 Accountancy Chapter 6 Important Extra Questions Accounting for Share Capital

Accounting for Share Capital Important Extra Questions Very Short Answer Type

Question 1.

What is meant by over subscription of shares? (CBSE Compt. 2019)

Answer:

Oversubscription of shares means that the company receives applications for more than the number of shares offered to the public for subscription.

Question 2.

What is meant by ‘par value’ of a share? (CBSE Compt. 2019)

Answer:

Par value is the nominal value or the face value of the share.

Question 3.

Is Reserve Capital a part of Unsubscribed Capital or Uncalled Capital? (CBSE Delhi 2018)

Answer:

Yes.

Question 4.

A company issued 25,000 equity shares of ₹ 10 each but received applications for.30,000 shares. Name the case of subscription.

Answer:

Over subscription

Question 5.

Neelam Limited has the following balances appearing in the balance sheet:

The company decided to redeem its 9% debentures at a premium of 10%. You are required to state how much securities premium amount can be used for redemption of debentures.

Answer:

₹ 12,00,000.

Question 6.

On 1.1.2016 the first call of ₹ 3 per share became due on 1,00,000 equity shares issued by Kamini Ltd. Karan a holder of 500 shares did not pay the first call money. Arjun a shareholder holding 1000 shares paid the second and final call of ₹ 5 per share along with the first call.

Pass the necessary journal entry for the amount received by opening ‘Calls-in-arrears’ and ‘Calls-in- advance’ account in the books of the company. (CBSE Outside Delhi 2016)

Answer:

Question 7.

Where will you show call in arrears in the balance sheet?

Answer:

As deduction from the subscribed but not fully paid share capital.

Question 8.

Where will you show call in advance in the balance sheet?

Answer:

It is shown under other current liabilities.

Question 9.

At what rate of interest, interest on call in arrears, is charged? .

Answer:

10%p.a.

Question 10.

At what rate interest on calls-in-advance is paid by the company according to Table F of Companies Act, 2013? ’ (CBSE Delhi Compt.2014)

Answer:

As per Table F, company is required to pay interest on the amount of calls in advance @ 12% p.a.

Question 11.

How would you deal in a situation where the value of purchase considerations is more than the value of net assets while acquiring a business? .

Answer:

It would refer to loss.

Question 12.

How will you deal in a situation where the value of net assets is more than the value of purchase consideration while acquiring a business?

Answer:

It would refer to gain .

Question 13.

Which account will you debit while issuing the shares to the promoters of a company against their services?

Answer:

Goodwill Account or Incorporation Expenses Account.

Question 14.

When can shares held by a shareholder be forfeited?. (CBSE Delhi 2017)

Answer:

On the non-payment of call money due.

Question 15.

A Ltd forfeited a share of 100 issued at a premium of 20% for non-payment of first call of 30 per share and’ final call of 10 per share. State the minimum price at which this share can be reissued. (CBSE Sample Paper 2016)

Answer:

₹ 40 per share!

Question 16.

Give the meaning of forfeiture of share.

Answer:

Cancellation of shares.

Question 17.

At the time of forfeiture of shares, what amount is credited to share forfeiture account?

Answer:

The amount already received.

Question 18.

Where will you show the share forfeited account in the balance sheet of a company?

Answer:

As an addition in the subscribed capital.

Question 19.

What amount of share capital is debited when the shares are forfeited?

Answer:

Called up money.

Question 20.

What amount of share capital is credited when the forfeited shares are reissued?

Answer:

Paid up capital of shares at the time of reissue.

Question 21.

Y Ltd. forfeited 100 equity shares of ₹ 10 each for the non-payment of first call of ₹ 2 per share. The final call of ₹ 2 per share was yet to be made.

Calculate the maximum amount of discount at which these shares can be re-issued. (CBSE Delhi 2017)

Answer:

₹ 6 per share or ₹ 600.

Question 22.

If a question is silent on the question of excess money received with application, how would you treat it?

Answer:

In the absence of any information, excess money over the amount due on allotment shall be refunded.

Accounting for Share Capital Important Extra Questions Short Answer Type

Question 1.

What is meant by ‘over-subscription’ of shares ? With the help of an example, briefly explain the alternatives available for allotment of shares in case of over-subscription. (CBSE Outside Delhi 2019)

Answer:

When the no. of shares applied is more than the no. of shares offered by the co., it is said to be case of over-subscription.

For Example: A company invited applications for 1,00,000 shares and received applications for 4,00,000 shares. Three alternatives are available for allotment of shares:

- To allot 1,00,000 shares in full to selected applicants and the remaining 3,00,000 applications were rejected outright.

- To make pro-rata allotment to all applicants.

- Totally reject applications for 2,00,000 shares, accept full applications for 80,000 shares and make pro-rata allotment for 20,000 shares to remaining 1,20,000 applicants.

Question 2.

What is meant by ‘Forfeiture of shares’ ₹ When does ‘gain on forfeited shares’ arise and when is it transferred to capital reserve ? (CBSE Outside Delhi 2019)

Answer:

Cancellation of shares for the non payment of called up amount is termed as Forfeiture of shares.

Gain on Forfeited shares arises on reissue.

It is transferred immediately on the reissue of forfeited shares.

Question 3.

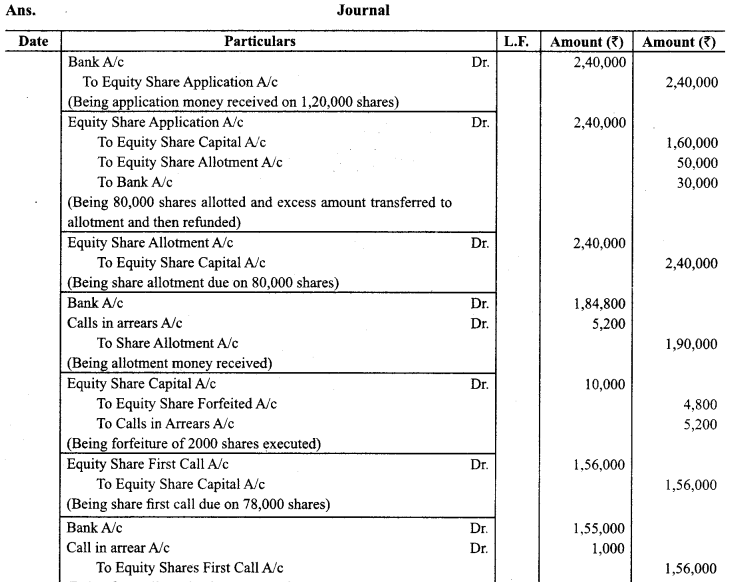

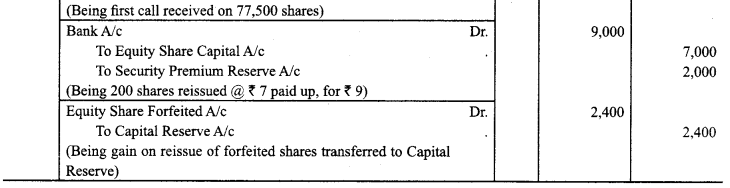

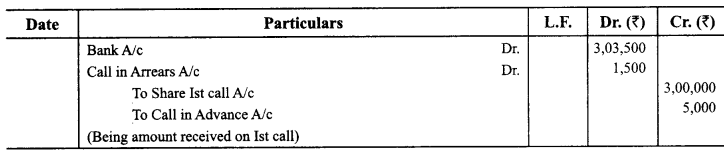

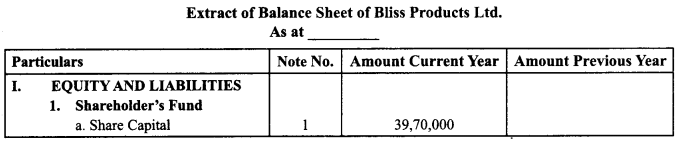

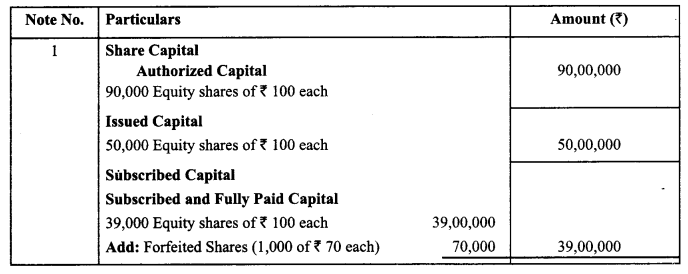

Bliss Products Ltd. registered with capital of ₹ 90,00,000 divided into 90,000 equity shares of₹ 100 each. The company issued prospectus inviting applications for 50,000 equity shares of ₹ 100 each payable as ₹ 20 on application, ₹ 30 on allotment, ₹ 20 on first call and balance on second call.

Applications were received for ₹ 40,000 shares. Raman to whom 1600 shares were allotted failed to pay final call money and these shares were forfeited. Of the forfeited shares, 600 shares were reissued to Sukhman, credited as fully paid for ₹ 90 per share.

Present the Share Capital as per Schedule III of Companies Act, 2013. (CBSE Sample Paper 2019-20)

Answer:

Question 4.

To provide employment to the youth and to develop the Naxal affected backward areas of Chattisgarh. X Ltd. decided to set-up a power plant. For raising funds the company decided to issue 7,50,000 equity shares of ₹ 10 each at a premium of 50%. The whole amount was payable on application. Application for 20,00,000 shares were received. Applications for 50,000 shares were rejected and shares were allotted to the remaining application on pro-rata basis.

Pass necessary journal entries for the above transactions in the books of the company.

(CBSE Outside Delhi 2016, Modified)

Answer:

Question 5.

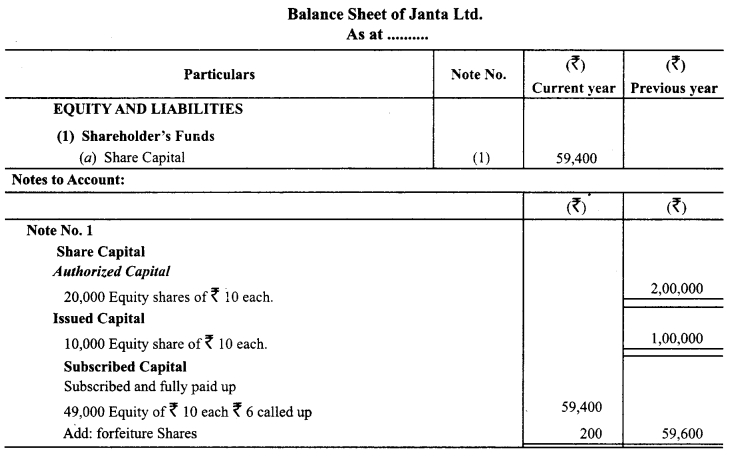

Janta Ltd. had an authorized capital of ₹ 2,00,000 divided into equity shares of ₹ 10 each. The company offered for subscription of ₹ 10,000 shares. The issue was fully subscribed. The amount payable on application was ₹ 2 per share. ₹ 4 per share were payable each on allotment and first and final call. A share holder holding 100 shares failed to pay the allotment money. His shares were forfeited. The company did not make the final call. How the ‘share capital’ will be presented in the company’s balance-sheet?

Also prepare Notes to Accounts for the same. (CBSE Sample paper 2014 Modified)

Answer:

Question 6.

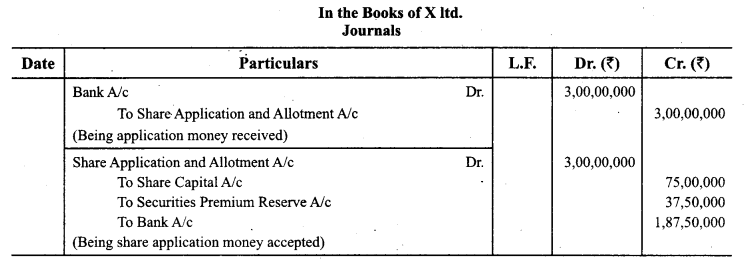

Drumbeats Ltd. had a prosperous shoe business. They were manufacturing shoes in India and exporting to Italy. Being a socially aware organization, they wanted to pay back to the society. They decided to not on supply free shoes to 50 orphanages in various parts of the country but also give employment to children from those orphanages who were above 18 years of age. In order to meet the fund requirements, they decided to raise 50,000 equity shares of ₹ 50 each and 40,000. 9% debentures of ₹ 40 each. Pass the necessary journe entries for issue to shares and debentures. (CBSE Sample Paper 2015, Modified)

Answer:

Question 7.

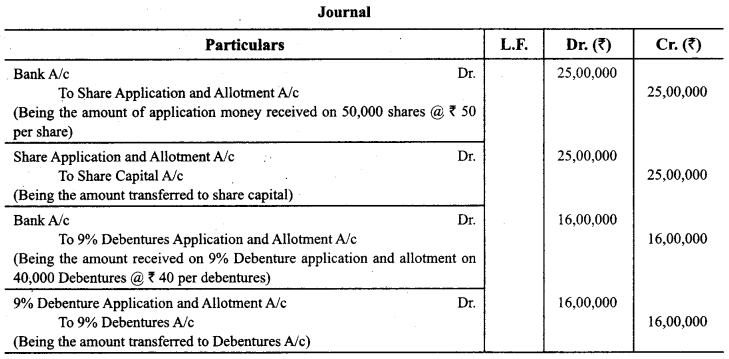

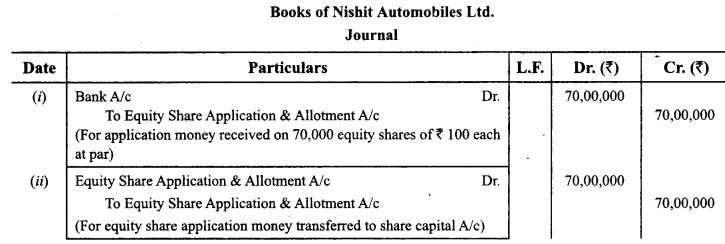

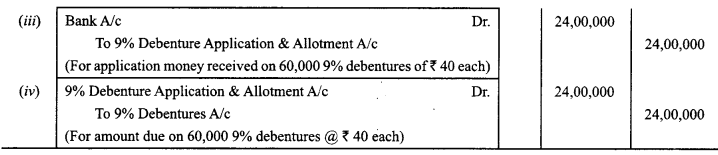

Nishit Automobiles Co. is an manufacture of low cost cars in India. It has a strong sales and distribution network spread across the country. It follows high standards in environmental safety in various processes of car manufacturing. It runs a school to provide quality education to the children of employees of the company and an ‘Adult Education Centre’ to help adults learn reading and writing and to acquire basis literacy. The company is doing well and anticipates a higher demand for its products in the future. For the same, it decides to set up a new manufacturing unit in a backward area of Orissa creating livelihood for people, especially those from disadvantaged sections of society in rural India. In order to raise fund requirements they decided to issue 70,000 equity shares of ₹ 100 each at par and 60,000. 9% Debentures of ₹ 40 each. Pass necessary Journal Entries for the issue of shares and 9% debentures in the books of the company and also identify.

Answer:

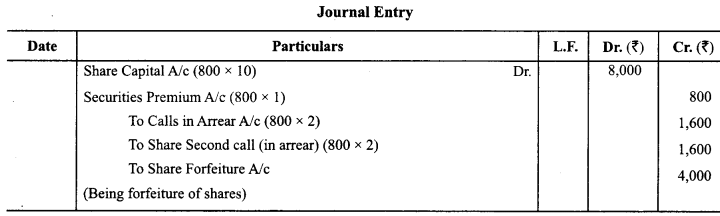

Question 8.

A Company forfeited 800 equity shares of ₹ 10 each issued at a discount of 10% for non-payment of two calls of ₹ 2 each. Calculate the amount forfeited by the company-and pass the journal entry for forfeiture of the shares.

Answer:

Question 9.

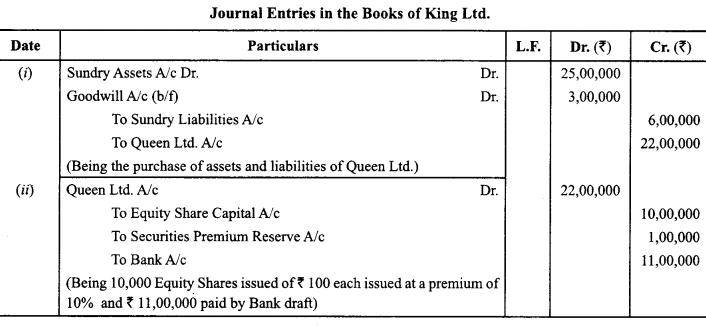

King Ltd took over Assets of 25,00,000 and liabilities of 6,00,000 of Queen Ltd. King Ltd paid the purchase consideration by issuing 10,000 equity shares of 100 each at a premium of 10% and 11,00,000 by Bank Draft.

Calculate Purchase consideration and pass necessary Journal entries in the books of King Ltd. (CBSE Sample Paper 2016, 2017)

Answer:

Calculation of Purchase Consideration:

Nominal Value of Shares issued = 10000 x ₹ 100 = ₹ 10,00,000

Securities Premium Reserve = ₹ 1,00,000

Bank draft = ₹ 11,00,000

Purchase consideration = ₹ 22,00,000

Question 10.

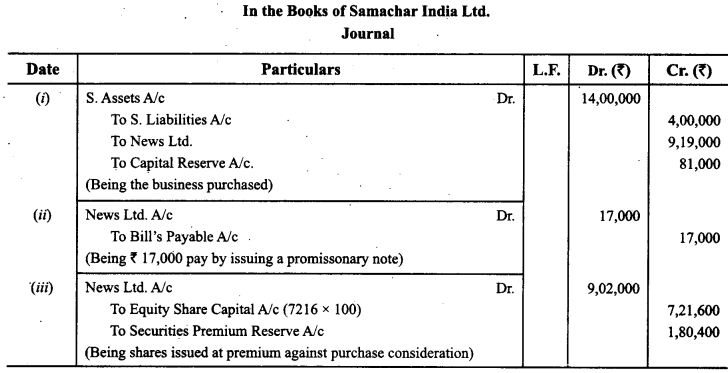

Samachar India Ltd. took over the assets of ₹ 14,00,000 and liabilities of ₹ 4,00,000 from News Ltd. for a purchase consideration of ₹ 9,19,000. Samachar India Ltd. issued a promissory note of ₹ 17,000 payable after 60 days in favour of News Ltd. and the balance amount was paid by issue of equity shares of ₹ 100 each at a premium of ₹ 25 per share.

Pas necessary Journal entries for the above transactions in the book of Samachar India Ltd. (CBSE Outside Delhi 2016)

Question 11.

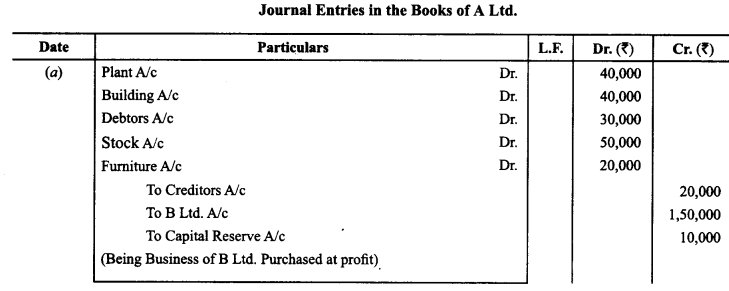

A Ltd. purchased a running business from B Ltd. for a sum of ₹ 1,50,000 payable by issue of 10,000 equity shares of ₹ 10 each at a premium of ₹ 2 per share and balance in cash. The assets and liabilities taken over were:

Plant – ₹ 40,000;

Building – ₹ 40,000;

Debtors – ₹ 30,000;

Stock – ₹ 50,000;

Furniture – ₹ 20,000;

Creditors – ₹ 20,000

You are required to pass necessary journal entries for the above transactions in the book of A Ltd.

(CBSE Delhi Compartment 2014)

Answer:

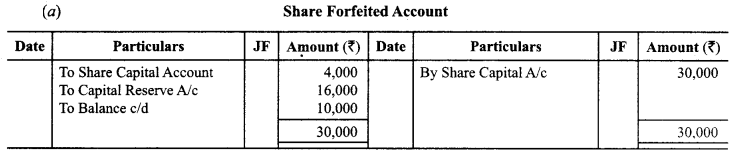

Question 12.

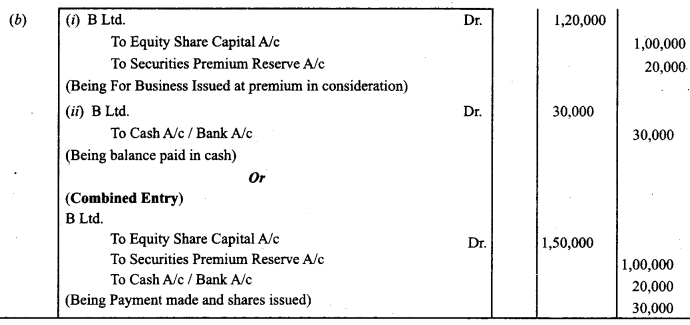

Prayuj Ltd. forfeited 2,000 shares of ₹ 10 each, fully called up, on which they had received only ₹ 14,000.50 of the forfeited shares were reissued for ₹ 9 per share fully paid up.

Pass necessary journal entries for forfeiture and re-issue of shares. Also prepare share forfeited account.

(Compt. Delhi 2017)

Question 13.

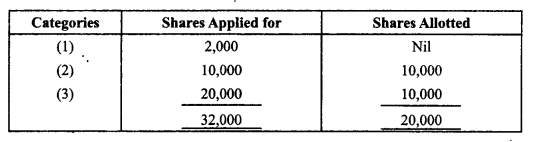

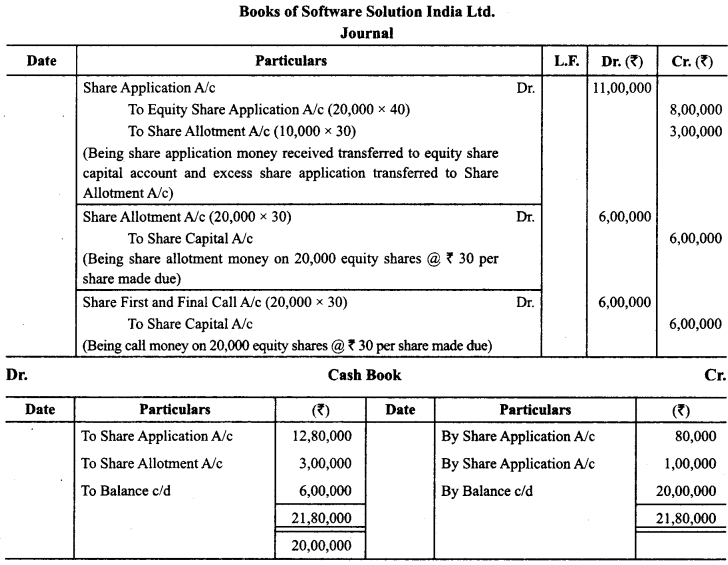

Software Solution India Ltd. inviting application for 20,000 equity share of ₹ 100 each, payable ₹ 40 on application. ₹ 30 on allotment and ₹ 30 on call. The company received applications for 32,000 shares. Applications for 2,000 shares were rejected and money returned to applicants. Applications for 10,000 shares were accepted in full and applicants for 20,000 share allotted half of the number of shares applied and excess application money adjusted into allotment. All money received due on allotment & call. Prepare journal and cash book.

Answer:

Accounting for Share Capital Important Extra Questions Long Answer Type

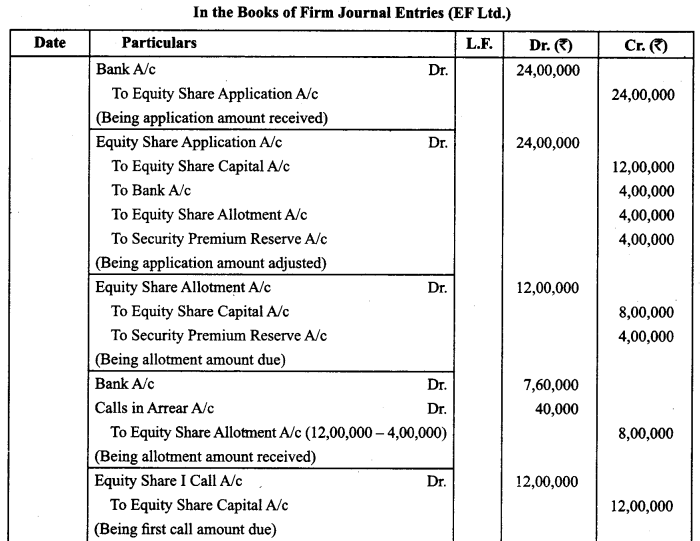

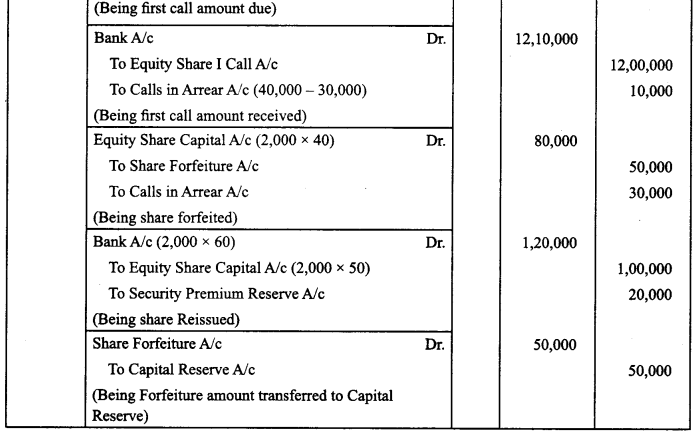

Question 1.

EF Ltd. invited applications for issuing 80,000 equity shares of ₹50 each at a premium of 20%. The amount was payable as follows:

On Application : ₹ 20 per share (including premium ₹ 5)

On Allotment : ₹ 15 per share (including premium ₹ 5)

On First Call : ₹ 15 per share

On Second and Final call : Balance amount

Applications for 1,20,000 shares were received. Applications for 20,000 shares were rejected and pro-rata allotment was made to the remaining applicants.

Seema, holding 4,000 shares failed to pay the allotment money. Afterwards the first call was made. Seema paid allotment money along with the first call. Sahaj who had applied for 2,500 shares failed to pay the first call money. Sahaj’s shares were forfeited and subsequently reissued to Geeta for ₹ 60 per share, ₹ 50 per share paid up. Final call was not made.

Pass necessary journal entries for the above transactions in the books of EF Ltd. by opening calls-in-arrears account. (CBSE Delhi 2019)

Answer:

Question 2.

S Ltd. invited applications for issuing 1,00,000 equity shares of ₹ 10 each. The shares were issued at a premium of ₹ 5 per share. The amount was payable as follows :

On Application and Allotment – ₹ 8 per share (including premium ₹ 3)

On the First and Final call – Balance including premium

Applications for 1,50,000 shares were received. Applications for 10,000 shares were rejected and pro-rata allotment was made to the remaining applicants on the following basis :

(I) Applicants for 80,000 shares were allotted 60,000 shares, and

(II) Applicants for 60,000 shares were allotted 40,000 shares.

Excess amount received on application and allotment was to be adjusted against sums due on call. X, who belonged to the first category and was allotted 300 shares, failed to pay the first and final call money. Y, who belonged to the second category and was allotted 200 shares, also failed to pay the first and final call money. Their shares were forfeited. The forfeited shares were reissued @ ₹ 12 per share as fully paid-up.

Pass necessary cash book and journal entries for the above transactions in the books of the company. (CBSE Outside Delhi 2019)

Answer:

Question 3.

Saregama Ltd invited applications for issuing 80,000 equity shares of ₹ 100 each at a premium of ₹ 10. The amount was payable as follows On Application – ₹ 30

On allotment – ₹ 30 (including a premium of ₹ 10)

On 1st call – ₹ 30

On Final Call Balance

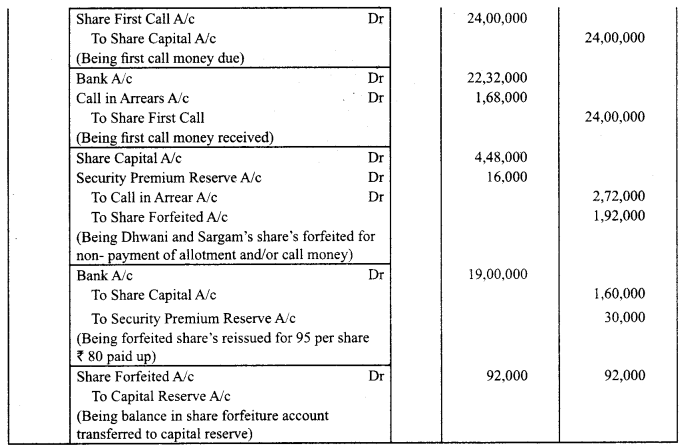

Applications of 1,20,000 shares were received. Allotment was made on pro rata basis to all applicants. Excess money received on application was adjusted on sums due on allotment. Dhwani, who was allotted 1,600 shares, failed to pay allotment money and Sargam who applied of 6,000 shares did not pay 1st call money. These shares were forfeited immediately after 1st call. 2,000 of these shares (including all shares of Dhwani were issued to Tarang for ₹ 95 per share as 80 paid up. Pass necessary journal entries in books of Saregama Ltd. by opening call in arrear, call in advance account, if final call has not been made. (CBSE Sample Paper 2019-20)

Answer:

Question 4.

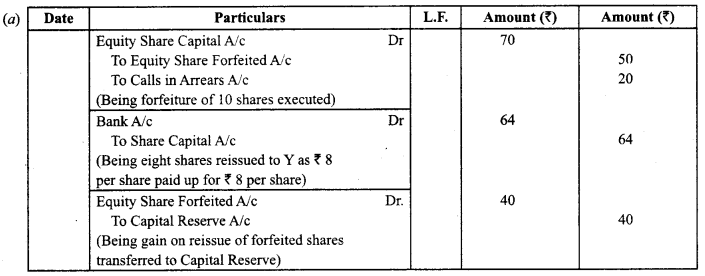

(a) X Ltd. forfeited 10 shares of ₹ 10 each, ₹ 7 called up on which the shareholder had paid application and allotment money of ₹ 5 per share. Out of these, 8 shares were re-issued to Y for ₹ 8 per share at ₹ 8 per paid up per share. Record the journal entries for forfeiture and reissue of shares by opening call in arrear, call in advance account.

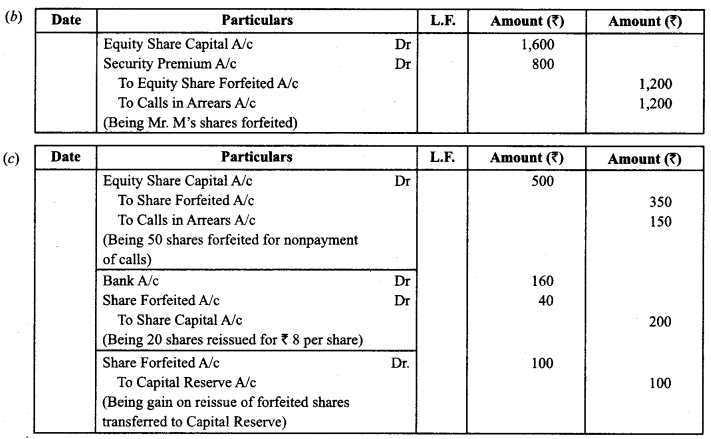

(b) L ltd forfeited Mr M’s shares who has applied for 600 shares and was allotted 400 shares failed to pay allotment money of ₹ 4 per share including premium of ₹ 2 on which he had paid application money of ₹ 2 only. Pass necessary journal entries for forfeiture of shares by opening call in arrear, call in advance account.

(c) Crown Ltd forfeited 50 shares of ₹ 10 each, for non-payment of final call money of ₹ 3 per share. Out of these 20 shares were reissued to Taj at ₹ 8 per share. Record the journal entries for forfeiture and reissue of shares assuming that the company maintains call in arrear, call in advance account. (CBSE Sample Paper 2019-20)

Answer:

Question 5.

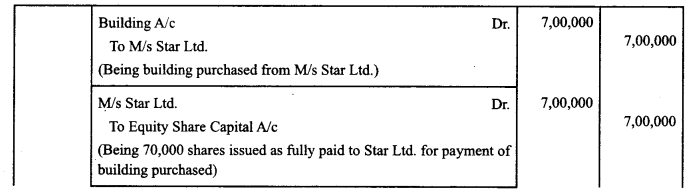

Venus Ltd’ was registered with an authorised capital of ₹ 40,00,000 divided into 4,00,000 equity shares of 10 each. 70,000 of these shares were issued as fully paid to ‘M/s. Star Ltd.’ for building purchased from them. 2,00,000 shares were issued to the public and the amounts were payable as follows:

On Application – ₹ 3 per share

On Allotment – ₹ 2 per share

On First Call – ₹ 2 per share

On Second and Final Call – ₹ 3 per share

The amounts received on these shares were as follows:

On 1,00,000 shares – Full amount called

On 60,000 shares – ₹ 1 per share

On 30,000 shares – ₹ 5 per share

On 10,000 shares – ₹ 3 per share

The directions forfeited 10,000 shares on which only ₹ 3 per share were received. These shares were reissued at ₹ 12 per share fully paid. Pass necessary journal entries for the above transactions in the books of ‘Venus Ltd’. (CBSE Compt. 2019)

Answer:

Question 6.

(a) AX Limited forfeited 6,000 shares of ₹ 10 each for non-payment of First call of ₹ 2 per share. The Final call of ₹ 3 per share was yet to be made. The Final call was made after Forfeited of these shares.. Of the forfeited shares, 4,000 shares were reissued at ₹ 9 per share as fully paid up. Assuming that the company maintains ‘Calls in Advance Account’ and ‘Calls in Arrears Account’, prepare “Share Forfeited Account” in the books of AX Limited.

(b) BG Limited issued 2,00,000 equity shares of₹ 20 each at a premium of ₹ 5 per share. The shares were allotted in the proportion of 5 : 4 of shares applied and allotted to all the applicants. Deepak, who had applied for 900 shares, failed to pay Allotment money of ₹ 7 per share (including premium) and on his failure to pay ‘First & Final Call’ of ₹ 2 per share, his shares were forfeited. 400 of the forfeited shares were reissued at ₹ 15 per share as fully paid up. Showing your working clearly, pass necessary Journal entries for the Forfeited and reissue of Deepak’s shares in the books of BG Limited. The company maintains‘Calls in Arrears’Account’.

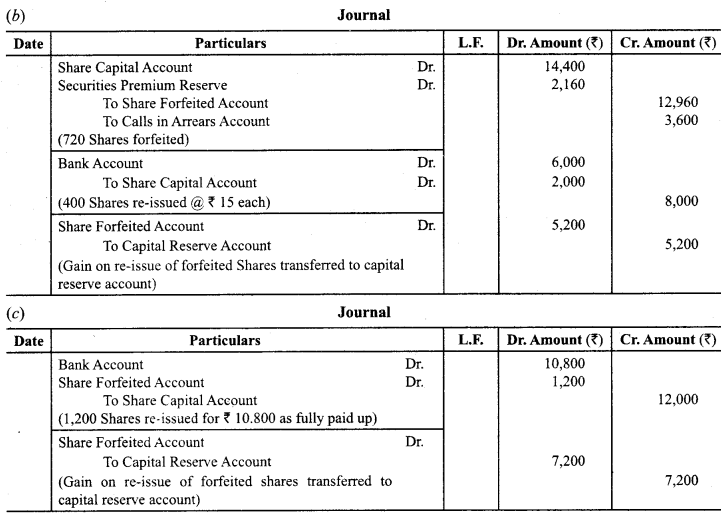

(c) ML Limited forfeited 1,200 shares of₹ 10 each allotted to Ravi for Non-payment of‘Second & Final Call’ of ₹ 5 per share (including premium of ₹ 2 per share). The forfeited shares were reissued for ₹ 10,800 as fully paid up. Pass necessary Journal entries for reissue of shares in the books of ML Limited. (CBSE Sample Paper 2017-18)

Answer:

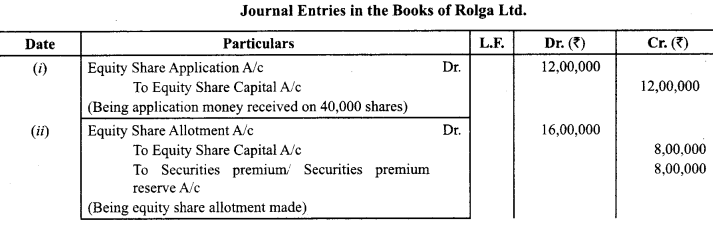

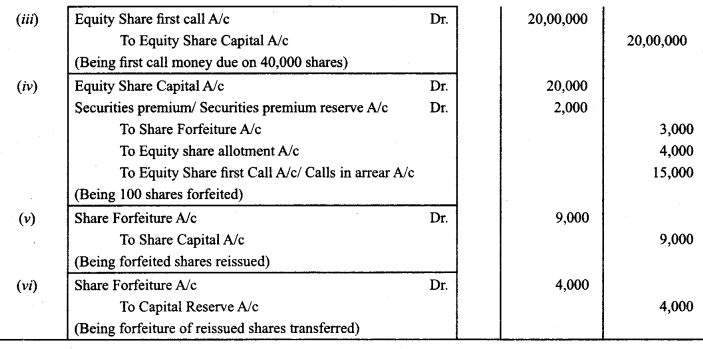

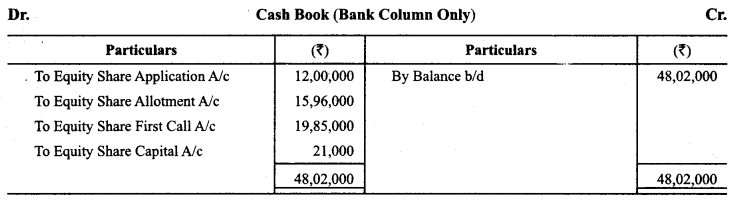

Question 7.

Rolga Ltd. is having an authorized capital of ₹ 50,00,000 divided into equity shares of ₹ 100 each. The company offered 42,000 shares to the public. The amount payable was as follows:

On Application – ₹ 30 per share

On Allotment – ₹ 40 per share (including premium)

On First and Final Call – ₹ 50 per share

Application were received for 40,000 shares.

All sums were duly received except the following:

Lai, a holder of 100 shares did not pay allotment and call money.

Pal, a holder of 200 shares did not pay call money.

The company forfeited the shares of Lai and Pal. Subsequently the forfeited shares were reissued for ₹ 70 per share as fully paid-up. Show the entries for the above transactions in the cash book and journal of the company. (CBSE Delhi Compartment 2015)

Answer:

Question 8.

X Ltd. invited application for issuing ₹ 50,000 equity shares of ₹ 10 each. The amount was payable as follows: On Application ₹ 2 per share on Allotment ₹ 2 per share on First Call ₹ 3 per share on Second Call Balance Amount.

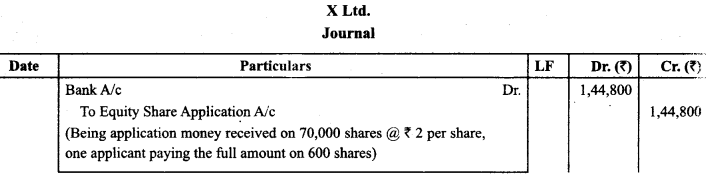

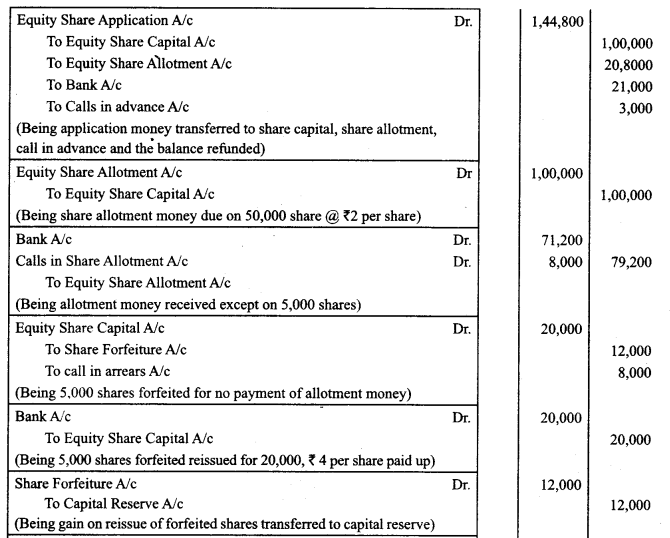

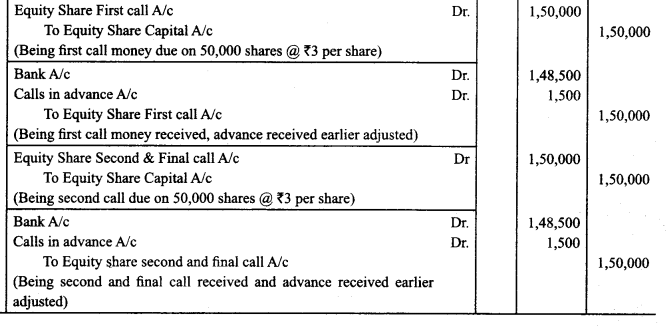

Applications for 70,000 shares were received. Applications for 10,000 shares were rejected and the application money was refunded. Shares were allotted to the remaining applicants on pro-rata basis and the excess money received on applications was transferred towards the sum due on allotment and calls (If any). Gopal who applied for 600 shares paid his entire share money with applications. Ghosh, who had applied for 6,000 shares failed to pay the allotment money and his shares were immediately forfeited. These forfeited shares were re-issued to Sultan for ₹ 20,000 ₹ 4 per share paid up. The first call money and the second call money was called and duly received. Pass the journal entry for the above transactions in the books of accounts of X Ltd. Open Calls in Arrear and Calls in Advance wherever necessary. (CBSE 2018)

Answer:

Question 9.

Khyati Ltd. issued a prospectus inviting applications for 80,000 equity shares of ₹ 10 each payable as follows:

₹2 on application

₹ 3 on allotment

₹ 2 on first call

₹ 3 on final call

Applications were received for 1,20,000 equity shares. It was decided to adjust the excess amount received on account of over subscription till allotment only. Hence allotment was made as under:

(i) To applicants for 20,000 shares – in full

(ii) To applicants for 40,000 shares – 10,000 shares

(iii) To applicants for 60,000 shares – 50,000 shares

Allotment was made and all shareholders except Tammana, who had applied for 2,400 shares out of the group (iii), could not pay allotment money. Her shares were forfeited immediately, after allotment. Another shareholder Chaya, who was allotted 500 shares out of group (ii), failed to pay first call. 50% of Tamanna’s shares were reissued to Satnaam as ₹ 7 paid up for payment of ₹ 9 per share.

Pass necessary journal entries in the books of Khyati Ltd. for the above transactions by opening calls in arrears and calls in advance account wherever necessary. (CBSE Sample Paper 2018-19)

Answer: