Check the below NCERT MCQ Questions for Class 12 Accountancy Chapter 3 Reconstitution of Partnership Firm: Admission of a Partner with Answers Pdf free download. MCQ Questions for Class 12 Accountancy with Answers were prepared based on the latest exam pattern. We have provided Reconstitution of Partnership Firm: Admission of a Partner Class 12 Accountancy MCQs Questions with Answers to help students understand the concept very well.

Class 12 Accountancy Chapter 3 Reconstitution of Partnership Firm: Admission of a Partner MCQ With Answers

Accountancy Class 12 Chapter 3 MCQs On Reconstitution of Partnership Firm: Admission of a Partner

Admission Of A Partner MCQ Chapter 3 Class 12 Question 1.

Goodwill is nothing more than probability that the old customer will resort to the old place. This definition of goodwill was given by:

(a) Spicer and Pegler

(b) ICAI

(c) Lord Elton

(d) AICPA

Answer

Answer: (c) Lord Elton

Admission Of Partner MCQ Chapter 3 Class 12 Question 2.

Goodwill is to be calculated at one and half year’ purchase of average profit of last 5 years. The firm earned profits during 3 years as ₹ 20,000 ₹ 18,000 and ₹ 9,000 and suffered losses of ₹ 2,000 and ₹5,000 in last 2 years. The amount of goodwill will be :

(a) ₹ 12,000

(b) ₹ 10,000

(c) ₹ 15,000

(d) None of these

Answer

Answer: (a) ₹ 12,000

MCQ Of Goodwill Class 12 Class 12 Question 3.

When there is no Goodwill Account in the books and goodwill is raised,…………….account will be debited :

(a) Partner’s Capital

(b) Goodwill

(c) Cash

(d) Reserve

Answer

Answer: (b) Goodwill

MCQ Questions For Class 12 Accountancy Chapter 3 Question 4.

The amount of goodwill is paid by new partner :

(a) for the payment of capital

(b) for sharing the profit

(c) for purchase of assets

(d) None of these

Answer

Answer: (b) for sharing the profit

MCQ On Admission Of A Partner Chapter 3 Class 12 Question 5.

At the time of admission of a new partners general reserve appearning in the old Balance Sheet is transferred to:

(a) All Partner’s Capital Accounts

(b) New Partner’s Capital Account

(c) Old Partners’. Capital Accounts

(d) None of these

Answer

Answer: (c) Old Partners’. Capital Accounts

MCQ Questions For Class 12 Accountancy Chapter Goodwill Question 6.

Profit or Loss on Revaluation is borne by:

(a) Old Partners

(b) New Partners

(c) All Partners

(d) Only Two Partners

Answer

Answer: (a) Old Partners

Admission Of Partner MCQ Pdf Chapter 3 Class 12 Question 7.

Share of goodwill brought by new partner in case is shared by old partners in :

(a) Sacrificing Ratio

(b) Old Ratio

(c) New Ratio

(d) Equal Ratio

Answer

Answer: (a) Sacrificing Ratio

Reconstitution Of Partnership Firm Class 12 MCQ Class 12 Question 8.

A, Band Care three partners sharing profits and losses in the ratio of 4:3:2. D is admitted for 1/10 share, the new ratio will be :

(a) 10 : 7 : 7 :4

(b) 5 : 3 : 2 : 1

(c) 4 : 3 : 2 : 1

(d) None of these

Answer

Answer: (c) 4 : 3 : 2 : 1

Question 9.

A and B are partners in a firm sharing profits in the ratio of 3:2. They admit C as a new partner for 1/3 rd share in the profits of the firm. The new profit sharing ratio of A, B and C would be :

(a) 3 : 2 : 1

(b) 3 : 2 : 2

(c) 3 : 2 : 3

(d) 6 : 4 : 5

Answer

Answer: (d) 6 : 4 : 5

Question 10.

X and Y are partners sharing profits in the ratio of 1:1. They admit Z for 1/5 th share who contributed ₹25,000 for his share of goodwill. The total value of goodwill of the firm will be :

(a) ₹ 2,50,000

(b) ₹ 50,000

(c) ₹ 1,00,000

(d) ₹ 1,25,000

Answer

Answer: (c) ₹ 1,00,000

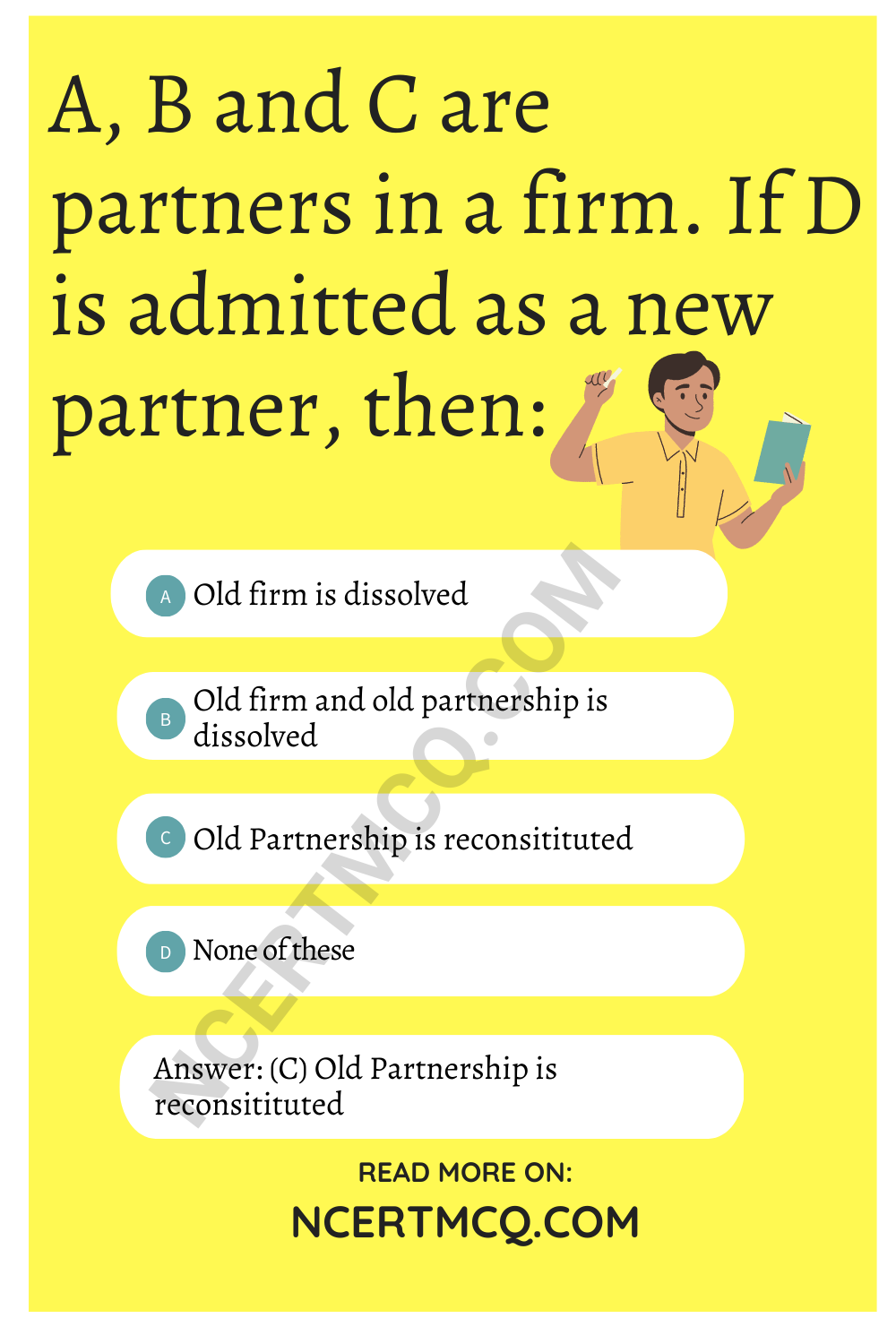

Question 11.

A, B and C are partners in a firm. If D is admitted as a new partner, then:

(a) Old firm is dissolved

(b) Old firm and old partnership is dissolved

(c) Old Partnership is reconsitituted

(d) None of these

Answer

Answer: (c) Old Partnership is reconsitituted

Question 12.

In which ratio, the cash brought in for goodwill by the new partner is shared by the existing partners :

(a) Profit sharing ratio

(b) Capital ratio

(c) Sacrificing ratio

(d) None of these

Answer

Answer: (c) Sacrificing ratio

Question 13.

Sacrificing ratio is ascertained at the time of:

(a) Death of a partner

(b) Retirement of a partner

(c) Admission of a partner

(d) None of these

Answer

Answer: (c) Admission of a partner

Question 14.

If at the time of admission of new partner, Profit and Loss Account balance appears in the books, it will the transferred to:

(a) Profit & Loss Appropriation A/c

(b) All Partners’ Capital A/cs

(c) Old Partners’ Capital A/cs

(d) Revaluation A/c

Answer

Answer: (c) Old Partners’ Capital A/cs

Question 15.

State the ‘true’ statement:

(a) Profit & Loss Adjustment A/c is prepared for revaluated of assets and liabilities on the admission of a partner

(b) The new partner is liable for the past losses of the firm

(c) In case the new partner is unable to bring in cash for goodwill, Goodwill Account may be raised in the firm’s books as per AS-26

(d) When a partner is admitted, there is dissolution of firm

Answer

Answer: (a) Profit & Loss Adjustment A/c is prepared for revaluated of assets and liabilities on the admission of a partner

Question 16.

Excess of the credit side over the debit side of Revaluation account is:

(a) Profit

(b) Loss

(c) Gain

(d) Expense

Answer

Answer: (a) Profit

Question 17.

Balance sheet prepared after new partnership agreement, assets and liabilities are recorded at:

(a) Original Value

(b) Revalued Figure

(c) At Realisable Value

(d) Either of (a) or (b)

Answer

Answer: (b) Revalued Figure

Question 18.

Assets and Liabilities are shown at their revalued values in :

(a) New Balance Sheet

(b) Revaluation A/c

(c) All Partner’s Capital A/c’s

(d) Realisation A/c

Answer

Answer: (a) New Balance Sheet

Question 19.

Which of the following assets is compulsorily revalued at the time of admission of a new partner :

(a) stock

(b) Fixed Assets

(c) Investment

(d) Goodwill

Answer

Answer: (d) Goodwill

Question 20.

A and B are partners. C is admitted with 1/5 share. C brings 7 1,20,000 as his share towards capital. The total net worth of the firm is :

(a) ₹ 1,00,000

(b) ₹ 4,00,000

(c) ₹ 1,20,000

(d) ₹ 6,00,000

Answer

Answer: (d) ₹ 6,00,000

Question 21.

A and B share profits and losses in the ratio of 3:4. C was admitted for 1/5 th share. New profit sharing ratio will be:

(a) 3 : 4 : 1

(b) 12 : 16 : 7

(c) 16 : 12 : 7

(d) None of these

Answer

Answer: (b) 12 : 16 : 7

Question 22.

The opening balance of Partner’s Capital Account is credited with:

(a) Interest on Capital

(b) Interest on Drawings

(c) Drawings

(d) Share in loss

Answer

Answer: (a) Interest on Capital

Question 23.

Share of goodwill brought in cash by the new partner is called:

(a) Assets

(b) Profit

(c) Premium

(d) None of these

Answer

Answer: (c) Premium

Question 24.

If the incoming partner brings the amount of goodwill in cash and also a balance exists in Goodwill A/c, then the Goodwill A/c is written off among the old partners:

(a) In new profit-sharing ratio

(b) In old profit-sharing ratio

(c) In sacrificing ratio

(d) In gaining ratio

Answer

Answer: (b) In old profit-sharing ratio

Question 25.

A and B share profits and losses in the ratio of 3 : 1.C is admitted into partnership for 1/4 share. The sacrificing ratio of A and B is :

(a) Equal

(b) 3 : 1

(c) 2 : 1

(d) 3 : 2

Answer

Answer: (b) 3 : 1

Question 26.

A and B are partners sharing profites in the ratio of 3 : 1. They admit C for 1/4 share in future profits. The new profit sharing ratio will be:

(a) A\(\frac {9}{16}\), B\(\frac {3}{16}\), C\(\frac {4}{16}\)

(b) A\(\frac {8}{16}\), B\(\frac {4}{16}\), C\(\frac {4}{16}\)

(c) A\(\frac {10}{10}\), B\(\frac {2}{16}\), C\(\frac {4}{16}\)

(d) A\(\frac {8}{16}\), B\(\frac {9}{16}\), C\(\frac {10}{16}\)

Answer

Answer: (a) A\(\frac {9}{16}\), B\(\frac {3}{16}\), C\(\frac {4}{16}\)

Question 27.

Formula of Sacrificing ratio is:

(a) New Ratio – Old Ratio

(b) Old Ratio – New Ratio

(c) Gain Ratio – Sacrificing Ratio

(d) New Ratio – Sacrificing Ratio .

Answer

Answer: (b) Old Ratio – New Ratio

Question 28.

The accumulated profits and reserves are transferred to:

(a) Realisation A/c

(b) Partner’s Capital A/cs

(c) Bank A/c

(d) Savings A/c

Answer

Answer: (b) Partner’s Capital A/cs

Question 29.

A, B and C are equal partners. D is admitted to the firm for non-ourth share. D brings ₹ 20,000 as capital and ₹ 5,000 being half of the premium for goodwill. The value of goodwill of the firm is :

(a) ₹ 10,000

(b) ₹ 40,000

(c) ₹ 30,000

(d) None of these

Answer

Answer: (b) ₹ 40,000

Question 30.

On the admission of a new partner, increase in the value of assets is debited to which account ?

(a) Revaluation Account

(b) Assets Account

(c) Old Partners’ Capital Accounts

(d) None of these

Answer

Answer: (b) Assets Account

Question 31.

Z is admitted in a firm for a 1/4 share in the profit for which he brings 7 30,000 for goodwill. It will be taken away by the old partners X and Y in :

(a) Old profit-sharing ratio

(b) New profit-sharing ratio

(c) Sacrificing ratio

(d) Capital ratio

Answer

Answer: (c) Sacrificing ratio

Question 32.

On the admission of a new partner, the decrease in the value of assets is debited to:

(a) Revaluation Account

(b) Assets Account

(c) Old Partners’ Capital Accounts

(d) None of these

Answer

Answer: (a) Revaluation Account

Question 33.

When the new partner pays for goodwill in cash, the amount should be debited in the firm’s book to:

(a) Goodwill Account

(b) Cash Account

(c) Capital Account of new partner

(d) None of these

Answer

Answer: (b) Cash Account

Question 34.

The balance of Revaluation Account or Profit & Loss Adjustment Account is transferred to Old Partners’ Capital Accounts in their :

(a) Old profit-sharing ratio

(b) New profit-sharing ratio

(c) Equal ratio

(d) Capital ratio

Answer

Answer: (a) Old profit-sharing ratio

Question 35.

X and Y share profits in the ratio of 3 : 2 Z was admitted as a partner who gets 1/5 share. Z acquires 3/20 from X and 1/20 from Y. The new profit sharing ratio will be :

(a) 9 : 7 : 4

(b) 8 : 8 : 4

(c) 6 : 10 : 4

(d) 10 : 6 :4

Answer

Answer: (a) 9 : 7 : 4

Question 36.

The opening balance of Partner’s Capital Account is credited with:

(a) Interest on Capital

(b) Interest on Drawings

(c) Drawings

(d) Share in loss

Answer

Answer: (a) Interest on Capital

Question 37.

At the time of admission of a new partner, Undistributed Profits appearing in the Balance Sheet of the old firm is transferred to the Capital Account of:

(a) Old partners is old profit-sharing ratio

(b) Old partners in new profit-sharing ratio

(c) All the partners in the new profit-sharing ratio

(d) None of these

Answer

Answer: (a) Old partners is old profit-sharing ratio

Question 38.

Z is admitted in a firm for al/4 share in the profit for which he brings 7 30,000 for goodwill. It will be taken away by the old partners X and Y in :

(a) Old profit-sharing ratio

(b) New profit-sharing ratio

(c) Sacrificing ratio

(d) Capital ratio

Answer

Answer: (c) Sacrificing ratio

Question 39.

General Reserval at the time of admission of a new partner is transferred to :

(a) Revaluation Account

(b) Old Partner’s Capital Account

(c) Profit and Loss Adjustment Account

(d) Realisation Account

Answer

Answer: (b) Old Partner’s Capital Account

Question 40.

Change in profit-sharing ratio of existing partners results in:

(a) Revaluation of Firm

(b) Reconstitutions of Firm

(c) Dissolution of Firm

(d) None of these

Answer

Answer: (b) Reconstitutions of Firm

Question 41.

X, Y and Z are partners in a firm, they divided profit and loss in the ratio of 4:3:1. They decided to share profit In the ratio 5:4:3. X’s and Y’s sacrifices are :

(a) \(\frac{2}{24}: \frac{1}{24}\)

(b) \(\frac{1}{24}: \frac{3}{24}\)

(c) \(\frac{2}{24}: \frac{3}{24}\)

(d) None of these

Answer

Answer: (a) \(\frac{2}{24}: \frac{1}{24}\)

Question 42.

On reconstitution of a partnership firm, recording of an unrecorded liability wil result in:

(a) Gain to the existing partners

(b) Loss to the existing partners

(c) Neither gain nor loss to the existing partners

(d) None of these

Answer

Answer: (b) Loss to the existing partners

Question 43.

Increase In the value of assets on reconstitution of the partnership firm results into :

(a) Gain to the existing partners

(b) Loss to the existing partners

(c) Neither gain nor loss to the existing partners

(d) None of these

Answer

Answer: (a) Gain to the existing partners

Question 44.

The balance of Revaluation Account is transferred to old Partner’s Capital Accounts in their:

(a) Old Profit-sharing Ratio

(b) New Profit-sharing Ratio

(c) Equal Ratio

(d) None of these

Answer

Answer: (a) Old Profit-sharing Ratio

Question 45.

X and Y share profits in the ratio 2 :3. In future they have decided to share profits in equal ratio. Which partner will sacrifice in which ratio ?

(a) X sacrifice 1/10

(b) Y sacrifice 1/5

(c) Y sacrifice 1/10

(d) None of these

Answer

Answer: (c) Y sacrifice 1/10

Question 46.

Change in the partnership agreement results in:

(a) Reconstitution of Firm

(b) Dissolution of Firm

(c) Amalgamation of Firm

(d) None of these

Answer

Answer: (a) Reconstitution of Firm

Question 47.

Change in the partnership agreement:

(a) Changes the relationship among the partners

(b) Results in end of partnership business

(c) Dissolves the partnership firm

(d) None of these

Answer

Answer: (a) Changes the relationship among the partners

Question 48.

Excess of credit side over the debit side in Revalution Account is:

(a) Profit

(b) Loss

(c) Receipt

(d) Expense

Answer

Answer: (a) Profit

Question 49.

A, B and C are partners in a firm, if D is admitted as a new partner:

(a) Old firm is dissolved

(b) Old firm and old partnership are dissolved

(c) Old partnership is reconstituted

(d) None of these

Answer

Answer: (c) Old partnership is reconstituted

Question 50.

Recording of an unrecorded asset on the reconstltutlam of a partnership firm will be:

(a) A gain to the existing partners

(b) A loss to the existing partners

(c) Neither a gain nor a loss to the existing partners

(d) None of these

Answer

Answer: (a) A gain to the existing partners

Question 51.

Revaluation Account or Profit & Loss Adjustment Account is a:

(a) Personal Account

(b) Real Account

(c) Nominal Account

(d) None of these

Answer

Answer: (c) Nominal Account

Question 52.

A, B, C and D are partners sharing their profits and losses equally. They change their profit sharing ratio to 2:2:1:1. How much will C sacrifice ?

(a) 1/6

(b) 1/12

(c) 1/24

(d) None of these

Answer

Answer: (d) None of these

Question 53.

Sacrificing Ratio:

(a) New Ratio – Old Ratio

(b) Old Ratio – New Ratio

(c) Gaining Ratio – Old Ratio

(d) Old Ratio – Gaining Ratio

Answer

Answer: (b) Old Ratio – New Ratio

Question 54.

Gaining Ratio:

(a) New Ratio – Old Ratio

(b) Old Ratio – Sacrificing Ratio

(c) New Ratio – Sacrificing Ratio

(d) Old Ratio – New Ratio

Answer

Answer: (a) New Ratio – Old Ratio

Question 55.

X and Y share profit and loss in 3:2. From 1st January, 2017 they agreed to share profit equally. Their sacrifice or gain will be :

(a) Sacrifice by X: 1/10

(b) Sacrifices by Y : 1/10

(c) Both (a) and (b)

(d) Non of these

Answer

Answer: (c) Both (a) and (b)

Question 56.

At the time of admission of a new partner, General Reserve a appearing in the old Balances Sheet is transferred to:

(a) All Partner’s Capital Accounts .

(b) New Partners’ Capital Accounts

(c) Old Partner’s Capital Accounts

(d) None of these

Answer

Answer: (c) Old Partner’s Capital Accounts

Question 57.

Change in profit-sharing ratio of existing partners results in:

(a) Revaluation of Firm

(b) Reconstitution of Firm

(c) Dissolution of Firm

(d) None of these

Answer

Answer: (b) Reconstitution of Firm

Question 58.

Generally the interest on capital is considered as :

(a) An appropriation of profit

(b) An Asset

(c) An Expense

(d) None of these

Answer

Answer: (a) An appropriation of profit

Question 59.

Increase in the value of assets on reconstitution of the partnership firm results into:

(a) Gain to the existing partners

(b) Loss to the existing partners

(c) Neither a gain nor a loss to the existing partners

(d) None of these

Answer

Answer: (a) Gain to the existing partners

Question 60.

Following are the factors affecting goodwill except:

(a) Nature of business

(b) Efficiency of Management

(c) Technical Knowledge

(d) Location of the Customers

Answer

Answer: (c) Technical Knowledge

Question 61.

The profit of the last three years are ₹ 42,000, ₹ 39,000 and ₹ 45,000. Value of goodwill at two years purchases of the average profits will be :

(a) ₹ 42,000

(b) ₹ 84,000

(c) ₹ 1,26,000

(d) ₹ 36,000

Answer

Answer: (b) ₹ 84,000

Question 62.

Under average profit basis goodwill is calculated by :

(a) No. of years’ purchased x Average profit

(b) No. of years’ purchased x Super profit

(c) Super Profit -r Expected Rate of Return

(d) None of these

Answer

Answer: (a) No. of years’ purchased x Average profit

Question 63.

Goodwill is:

(a) Tangible Asset

(b) Intangible Asset

(c) Current Asset

(d) None of these

Answer

Answer: (b) Intangible Asset

Question 64.

An asset which is not ficitious but intangible in nature, having realisable value is :

(a) Machinery

(b) Building

(c) Furniture

(d) Goodwill

Answer

Answer: (d) Goodwill

Question 65.

Which of the following is not a method of valuation of Goodwill:

(a) Revaluation Method

(b) Average Profit Method

(c) Super Profit Method

(d) Capitalisation Method

Answer

Answer: (a) Revaluation Method

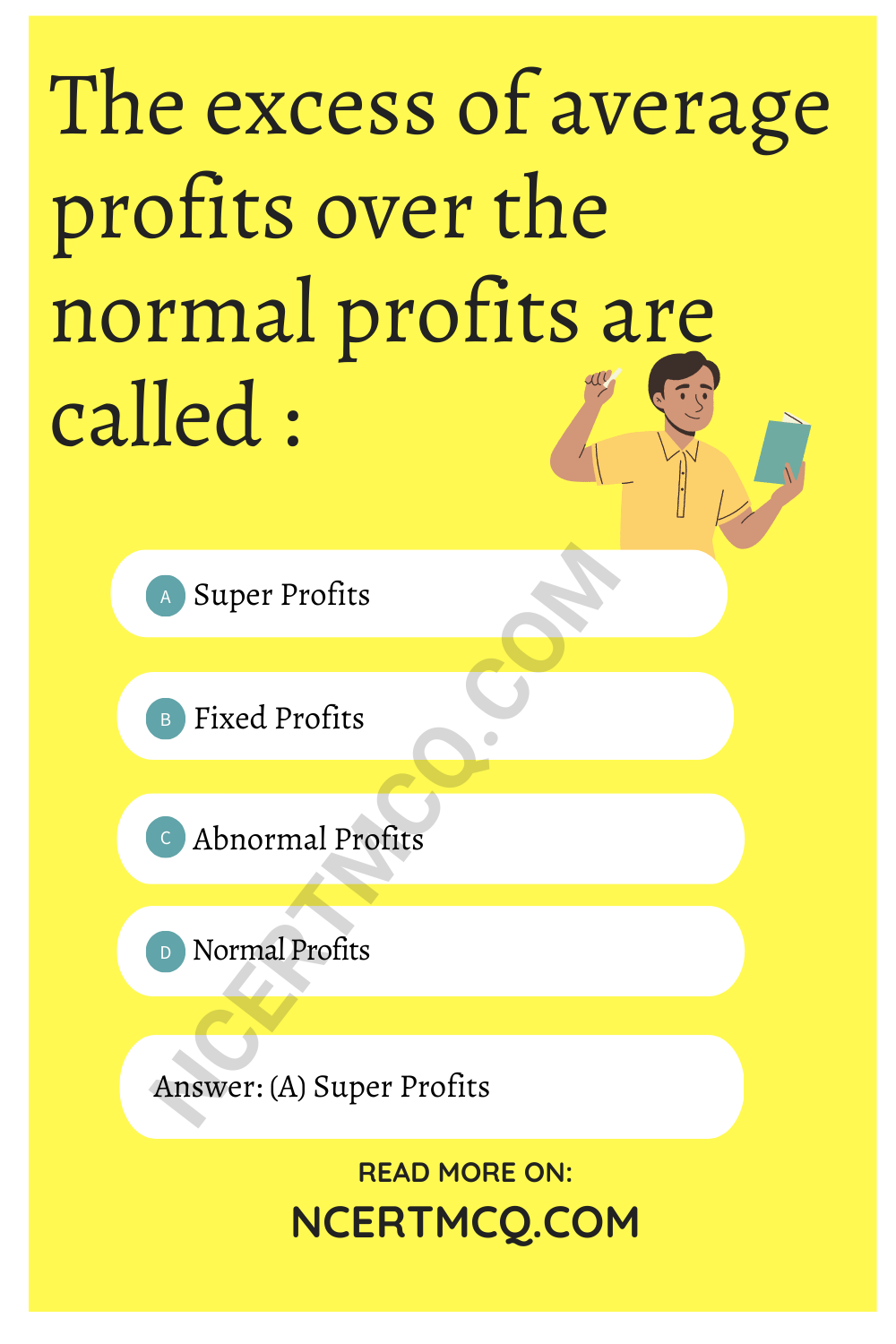

Question 66.

The excess of average profits over the normal profits are called :

(a) Super Profits

(b) Fixed Profits

(c) Abnormal Profits

(d) Normal Profits

Answer

Answer: (a) Super Profits

Question 67.

Goodwill is a…………….asset

(a) Useless

(b) Tangible

(c) Worthless

(d) Valuable

Answer

Answer: (c) Worthless

Question 68.

Under super profit basis goodwill is calculated by :

(a) No. of years’ purchased x Average Profit

(b) No. of years’ purchased x Super profit

(c) Super profit -r Expected rate of return

(d) None of these

Answer

Answer: (b) No. of years’ purchased x Super profit

Question 69.

Profits of the last three years were ₹ 6,000, ₹ 13,000 and ₹ 8,000 respectively. Goodwill at two years purchase of the average net profit will be :

(a) ₹ 81,000

(b) ₹ 27,0000

(c) ₹ 9,000

(d) ₹ 18,000

Answer

Answer: (d) ₹ 18,000

Question 70.

What do you mean by Super Profit ?

(a) Total Profit/No. of Years

(b) Average Profit – Normal Profit

(c) Weighted Profit/No. of Years’ Purchase

(d) None of these

Answer

Answer: (b) Average Profit – Normal Profit

Question 71.

Capital employed in a business is ₹ 1,50,000. Profits are ₹ 50,000 and the normal rate of profit is 20%. The amount of goodwill as per capitalisation method will be:

(a) ₹ 2,00,000

(b) ₹ 1,50,000

(c) ₹ 3,00,000

(d) ₹ 1,00,000

Answer

Answer: (d) ₹ 1,00,000

Question 72.

Weighted average method of calculating goodwill is used when:

(a) Profits are equal

(b) Profit has increasing trend

(c) Profit has decreasing trend

(d) Either (b) or (c)

Answer

Answer: (d) Either (b) or (c)

Question 73.

The monetary value of reputation of the business is called:

(a) Goodwill

(b) Super Profit

(c) Surplus

(d) Abnormal Profit

Answer

Answer: (a) Goodwill

Question 74.

A firm has an average profit of ₹ 60,000 Rate of return on capital employed is 12.5% p.a. Total capital employed in the firm was ₹ 4,00,000. Goodwill on the basis of two years purchase of super profit is :

(a) ₹ 20,000

(b) ₹ 15,000

(c) ₹ 10,000

(d) None of these

Answer

Answer: (a) ₹ 20,000

Question 75.

Under capitalisation method, goodwill is calculated by :

(a) Average Profit x No. of Years’ Purchase

(b) Super Profit x No. of Years’ Purchase

(c) Total of the discounted value of expected future benefits

(d) Super Profit -r Expected Rate of Return

Answer

Answer: (d) Super Profit -r Expected Rate of Return

Question 76.

“Goodwill is nothing more than probability that the old customer will resort to the old place.” This definition of goodwill was given by :

(a) Spicer and Pegler

(b) ICAI

(c) Lord Eldon

(d) AICPA

Answer

Answer: (c) Lord Eldon

Question 77.

What will be the value of goodwill at twice the average of last three years profit if the profits of the last three years were ₹ 4,000, ₹ 5,000 and ₹ 6,000 ?

(a) ₹ 5,000

(b) ₹ 10,000

(c) ₹ 8,000

(d) None of these

Answer

Answer: (b) ₹ 10,000

Question 78.

The Valuation of Goodwill is not necessary in Sole Trading:

(a) On selling the Firm

(b) On making a partner

(c) On estimation of Assets

(d) On Closing the Firm

Answer

Answer: (d) On Closing the Firm

We hope the given NCERT MCQ Questions for Class 12 Accountancy Chapter 3 Reconstitution of Partnership Firm: Admission of a Partner with Answers Pdf free download will help you. If you have any queries regarding CBSE Class 12 Accountancy Reconstitution of Partnership Firm: Admission of a Partner MCQs Multiple Choice Questions with Answers, drop a comment below and we will get back to you soon.

Class 12 Accountancy MCQ:

- Accounting for Not for Profit Organisation Class 12

- Accounting for Partnership: Basic Concepts Class 12

- Reconstitution of Partnership Firm: Admission of a Partner Class 12

- Reconstitution of Partnership Firm: Retirement / Death of a Partner Class 12

- Dissolution of a Partnership Firm Class 12

- Accounting for Share Capital Class 12

- Issue and Redemption of Debentures Class 12

- Financial Statements of a Company Class 12

- Analysis of Financial Statements Class 12

- Accounting Ratios Class 12

- Cash Flow Statement Class 12