Check the below NCERT MCQ Questions for Class 12 Accountancy Chapter 6 Accounting for Share Capital with Answers Pdf free download. MCQ Questions for Class 12 Accountancy with Answers were prepared based on the latest exam pattern. We have provided Accounting for Share Capital Class 12 Accountancy MCQs Questions with Answers to help students understand the concept very well.

Class 12 Accountancy Chapter 6 Accounting for Share Capital MCQ With Answers

Accountancy Class 12 Chapter 6 MCQs On Accounting for Share Capital

Share Capital MCQs Class 12 Chapter 6 Question 1.

Reserve share capital means :

(a) Part of authorised capital to be called at the beginning

(b) Portion of uncalled capital to be called only at liquidation

(c) Over subscribed capital

(d) Under subscribed capital

Answer

Answer: (b) Portion of uncalled capital to be called only at liquidation

Accounting For Share Capital MCQ Chapter 6 Question 2.

When full amount is due on any call but it is not received, then the short fall is debited to :

(a) Calls-in-advance

(b) Calls-in-arrear

(c) Share Capital

(d) Suspense Account

Answer

Answer: (b) Calls-in-arrear

Accounting For Share Capital Class 12 MCQ Chapter 6 Question 3.

The difference between subscribed capital and called up capital is called :

(a) Calls-in-arear

(b) Calls-in-advance

(c) Uncalled capital

(d) None of these

Answer

Answer: (c) Uncalled capital

Share Capital Class 12 MCQ Chapter 6 Question 4.

Which statement is issued before the issue of shares ?

(a) Prospectus

(b) Articles of Association

(c) Memorandum of Association

(d) All of these

Answer

Answer: (d) All of these

Share Capital Of A Company Means MCQ Chapter 6 Question 5.

Company can utilise securities premium for :

(a) Writing off loss incurred on revaluation of asset

(b) Issuing fully paid bonus shares

(c) Paying divided

(d) Writing off trading loss

Answer

Answer: (b) Issuing fully paid bonus shares

MCQ Of Share Capital Class 12 Chapter 6 Question 6.

When a company issues fully paid shares to promoters

for their services, the journal entry will be:

(a) Bank A/c Dr.

To Share Capital A/c

(b) Good will A/c Dr.

To Share Capital A/c

(c) Promoters Personal A/c Dr.

To Share Capital A/c

(d) Promotion Expenses A/c Dr.

To Share Capital A/c

Answer

Answer: (b) Goodwill A/c Dr.

To Share Capital A/c

Accounting For Share Capital MCQs Class 12 Chapter 6 Question 7.

When a company issues shares at a premium, amount of premium may be received by the company :

(a) Along with application money

(b) Along with application money

(c) Along with calls

(d) Along with any of the above

Answer

Answer: (d) Along with any of the above

MCQs Of Share Capital Class 12 Chapter 6 Question 8.

Share Application Account is :

(a) Personal Account

(b) Real Account

(c) Nominal/ Account

(d) None of these

Answer

Answer: (a) Personal Account

Issue Of Shares Class 12 MCQ Chapter 6 Question 9.

Secrities Premium can not be applied :

(a) For paying dividend to members

(b) For issuing bonus shares to members

(c) For writing off preliminary expenses of company

(d) For writing off discount on issue of debentures

Answer

Answer: (a) For paying dividend to members

Accounting For Shares Class 12 MCQ Chapter 6 Question 10.

A joint stock company is :

(a) An artificial legal person

(b) Natural person

(c) A general person

(d) None of these

Answer

Answer: (a) An artificial legal person

Share Capital MCQ Questions Chapter 6 Question 11.

Equity shareholders are :

(a) Customers

(b) Creditors

(c) Debtors

(d) Owners

Answer

Answer: (d) Owners

Share Capital Of A Company Means MCQ Answer Chapter 6 Question 12.

Reserve capital means :

(a) A part of subscribed uncalled capital

(b) Reserve Profit

(c) A part of Capital Reserve

(d) A part of Capital Redemption Reserve

Answer

Answer: (a) A part of subscribed uncalled capital

Question 13.

Securities Premium is shown under which head in the Balance Sheet ?

(a) Reserve and Surplus

(b) Miscellaneous Expenditure

(c) Current Liabilities

(d) Share Capital

Answer

Answer: (a) Reserve and Surplus

Question 14.

Shares may be issued :

(a) At par value

(b) At FYemimum

(c) At Discount

(d) Both (a) & (b)

Answer

Answer: (d) Both (a) & (b)

Question 15.

Capital included in the liabilities of a company is called :

(a) Authorised Capital

(b) Issued Capital

(c) Subscribed Capital

(d) Paid-up Capital

Answer

Answer: (d) Paid-up Capital

Question 16.

An issue of shares which is not a public issue but offered to a selected group of persons is called :

(a) Public offer

(b) Private placement of shares

(c) Initial public offer

(d) None of these

Answer

Answer: (d) None of these

Question 17.

If a share of ₹ 10 on which ₹ 8 has been called and ₹ 6 is paid is forfeited, the Share Capital Account should be debited with :

(a) ₹ 8

(b) ₹ 10

(c) ₹ 6

(d) ₹ 2

Answer

Answer: (a) ₹ 8

Question 18.

When shares are forfeited, the Share Capital Account is debited with:

(a) Nominal value of Shares

(b) Market value of Shares

(c) Called-up value of Shares

(d) Paid-up value of Shares

Answer

Answer: (c) Called-up value of Shares

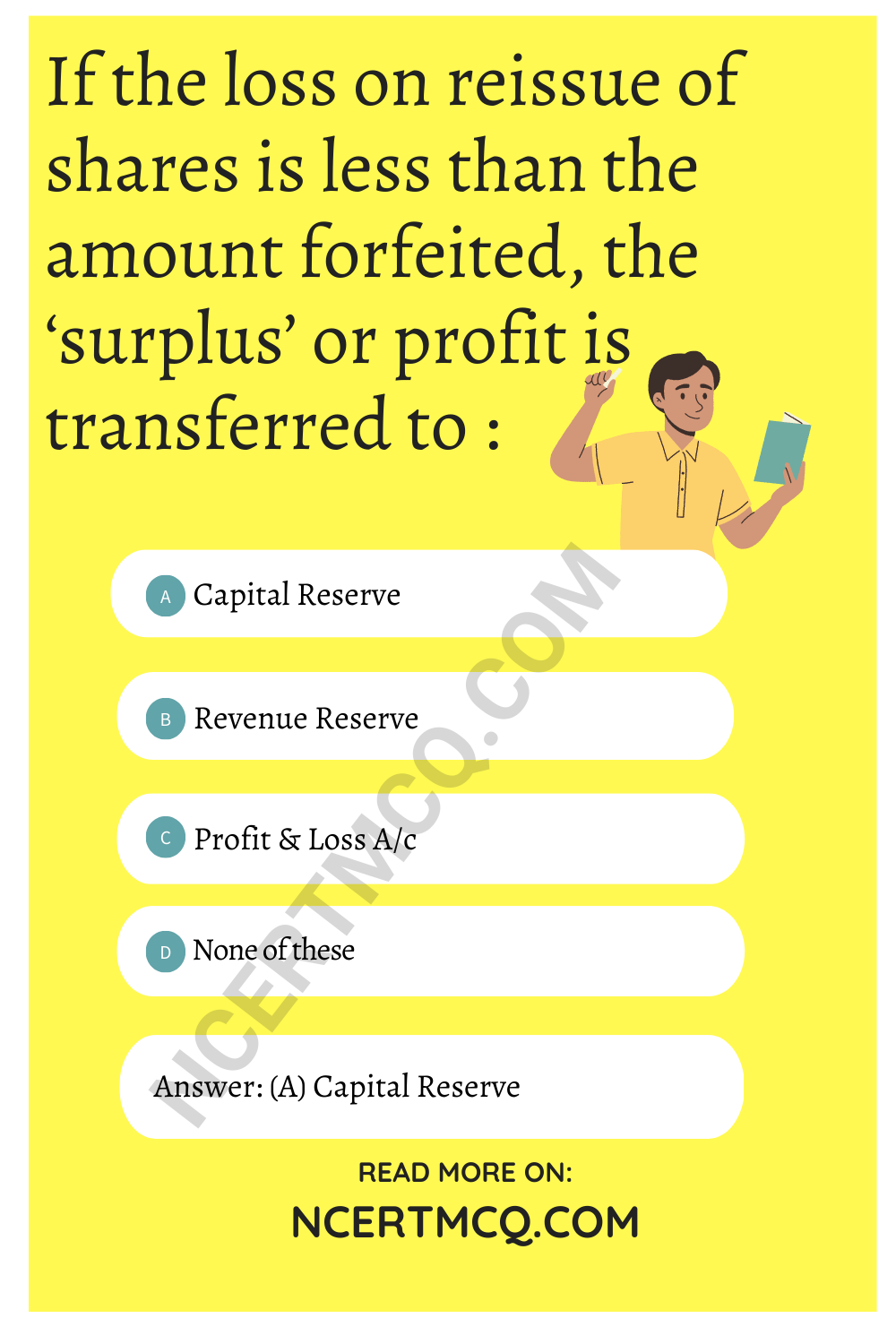

Question 19.

If the loss on reissue of shares is less than the amount forfeited, the ‘surplus’ or profit is transferred to :

(a) Capital Reserve

(b) Revenue Reserve

(c) Profit & Loss A/c

(d) None of these

Answer

Answer: (a) Capital Reserve

Question 20.

J. Ltd. re-issue 2,000 shares which where forfeited by crediting share forfeiture account by ₹ 3,000. These shares were re-issued at ₹ 9 per share. The amount transferred to capital reserve will be :

(a) ₹ 3,000

(b) ₹ 2,000

(c) ₹ 1000

(d) Nil

Answer

Answer: (c) ₹ 1000

Question 21.

If a share of ₹ 10 on which ₹ 8 has been paid up is forfeited, it can be reissued at the minimum price of…….

(a) 10 Rs. per share

(b) 8 Rs. per share

(c) 5 Rs. per share

(d) 2 Rs. per share

Answer

Answer: (d) 2 Rs. per share

Question 22.

Z & Co. forfeited 100 shares of 10 Rs. each for non-payment of final call of 2 Rs. per share. All the forfeited shares were re-issued at 9 Rs. per share. What amount will be transferred to Capital Reserve A/c ?

(a) 700 Rs.

(b) 800 Rs.

(c) 900 Rs.

(d) 1,000 Rs.

Answer

Answer: (a) 700 Rs.

Question 23.

Forfeiture of shares results in the reduction of:

(a) Paid-up Capital

(b) Authorised Capital

(c) Fixed Assets

(d) Reserve Capital

Answer

Answer: (a) Paid-up Capital

Question 24.

Amount of calls in Arrear is :

(a) Added to capital

(b) Deducted from share capital

(c) Shown on the assets side

(d) Shown an the equity and liability side

Answer

Answer: (b) Deducted from share capital

Question 25.

Discount allowed on reissue of forfeited shares is debited to:

(a) Share Capital A/c

(b) Share Forfeiture A/c

(c) Profit & Loss A/c

(d) General Reserve A/c

Answer

Answer: (b) Share Forfeiture A/c

Question 26.

A company has…………

(a) Separate Legal Entity

(b) Perpetual Existence

(c) Limited Liability

(d) All the above

Answer

Answer: (d) All the above

Question 27.

The liability of members in a company is :

(a) Limited

(b) Unlimited

(c) Stable

(d) Fluctuating

Answer

Answer: (a) Limited

Question 28.

Equity shareholders are :

(a) Creditors of the company

(b) Owners of the company

(c) Customers of the company

(d) None of these

Answer

Answer: (b) Owners of the company

Question 29.

Balance of Forfeited Shares Account after reissue of forfeited shares is transferred to :

(a) Profit & Loss A/c

(b) Capital Reserve Account

(c) General Reserve Account

(d) None of these

Answer

Answer: (b) Capital Reserve Account

Question 30.

Under the provisions of Companies Act, company can issue:

(a) Only equity shares

(b) Only preference shares

(c) Preference shares and equity shares

(d) None of these

Answer

Answer: (c) Preference shares and equity shares

Question 31.

Reight shares are the shares, which :

(a) Are issued to the Direction of the company

(b) Are issued to existing shareholders of the company

(c) Are issued to promoters in consideration of their services

(d) Are issued to the vendors for purchasing assets

Answer

Answer: (b) Are issued to existing shareholders of the company

Question 32.

Total amount of liabilities side includes :

(a) Authorised Capital

(b) Issued Capital

(c) Subscribed Capital

(d) Paid-up Capital

Answer

Answer: (d) Paid-up Capital

Question 33.

A company issues its shares at premium under which Section of Indian Companies Act, 2013 ?

(a) 78

(b) 79

(c) 52

(d) 53

Answer

Answer: (c) 52

Question 34.

Shares can be forfeited :

(a) For failure to attend meetings

(b) For non-payment of call money

(c) For failure to repay the loan to the Bank

(d) For which shares are pledged as a security

Answer

Answer: (b) For non-payment of call money

Question 35.

Shareholders get:

(a) Interest

(b) Dividend

(c) Commission

(d) Profit

Answer

Answer: (b) Dividend

Question 36.

According to Table E of the Companies Act, 2013 interest on calls in arrears charged should not exceed :

(a) 5% p.a.

(b) 6% p.a.

(c) 8%p.a.

(d) 10%p.a.

Answer

Answer: (d) 10%p.a.

Question 37.

Premium on issue of shares is a :

(a) Capital Gain

(b) Capital Loss

(c) General Profit

(d) General Loss

Answer

Answer: (a) Capital Gain

Question 38.

Premium on issue of shares is shown on which side of the Balance sheet.

(a) Assets

(b) Liabilities

(c) Both

(d) None of these

Answer

Answer: (b) Liabilities

Question 39.

Share Allotment Account is :

(a) Personal A/c

(b) Real A/c

(c) Nominal A/c

(d) None of these

Answer

Answer: (a) Personal A/c

Question 40.

The portion of the authorised capital which can be called-up only on the liquidation of the company is called:

(a) Issued Capital

(b) Called-up Capital

(c) Uncalled Capital

(d) Reserve Capital

Answer

Answer: (d) Reserve Capital

Question 41.

Premium on issue of shares can be used for :

(a) Issue of Bonus shares

(b) Distribution of Profit

(c) Transferring to General Reserve

(d) All these

Answer

Answer: (a) Issue of Bonus shares

Question 42.

If equity share of ₹ 10 Rs. each is issued at ₹ 12 each, it is called:

(a) Issued at Par

(b) Issued at Premium

(c) Issued at Discount

(d) None of these

Answer

Answer: (b) Issued at Premium

Question 43.

The maximum capital beyond which a company is not allowed to raise funds, by issue of shares is called …………..

(a) Issued capital

(b) Reserve capital

(c) Authorised capital

(d) Subscribed capital

Answer

Answer: (b) Reserve capital

Question 44.

As per Table F the maximum rate of interest on calls in advance paid is:

(a) 8% p.a.

(b) 12% p.a.

(c) 5 % p.a.

(d) None of these

Answer

Answer: (b) 12% p.a.

Question 45.

As per the Companies Act, only preference shares, which are redeemable within …………. can be issued.

(a) 24 years

(b) 22 years

(c) 30 years

(d) 20 years

Answer

Answer: (d) 20 years

Question 46.

Which one of the following is the registered capital of the company ?

(a) Paid-up capital

(b) Uncalled capital

(c) Authorised capital

(d) Issued capital

Answer

Answer: (c) Authorised capital

Question 47.

Dividends are usually paid on :

(a) Authorised Capital

(b) Issued Capital

(c) Called-up Capital

(d) Paid-up Capital

Answer

Answer: (d) Paid-up Capital

Question 48.

If vendors are issued fully paid shares of ₹ 1,00,000 in consideration of net assets of ₹ 1,20,000 the balance of ₹ 20,000 will be credited to :

(a) Goodwill Account

(b) Capital Reserve Account

(c) Vendor’s Account

(d) Profit & Loss Account

Answer

Answer: (b) Capital Reserve Account

Question 49.

Which account should be debited when shows an issued to promoters:

(a) Share Capital A/c

(b) Assets A/c

(c) Promoter’s A/c

(d) Goodwill A/c

Answer

Answer: (d) Goodwill A/c

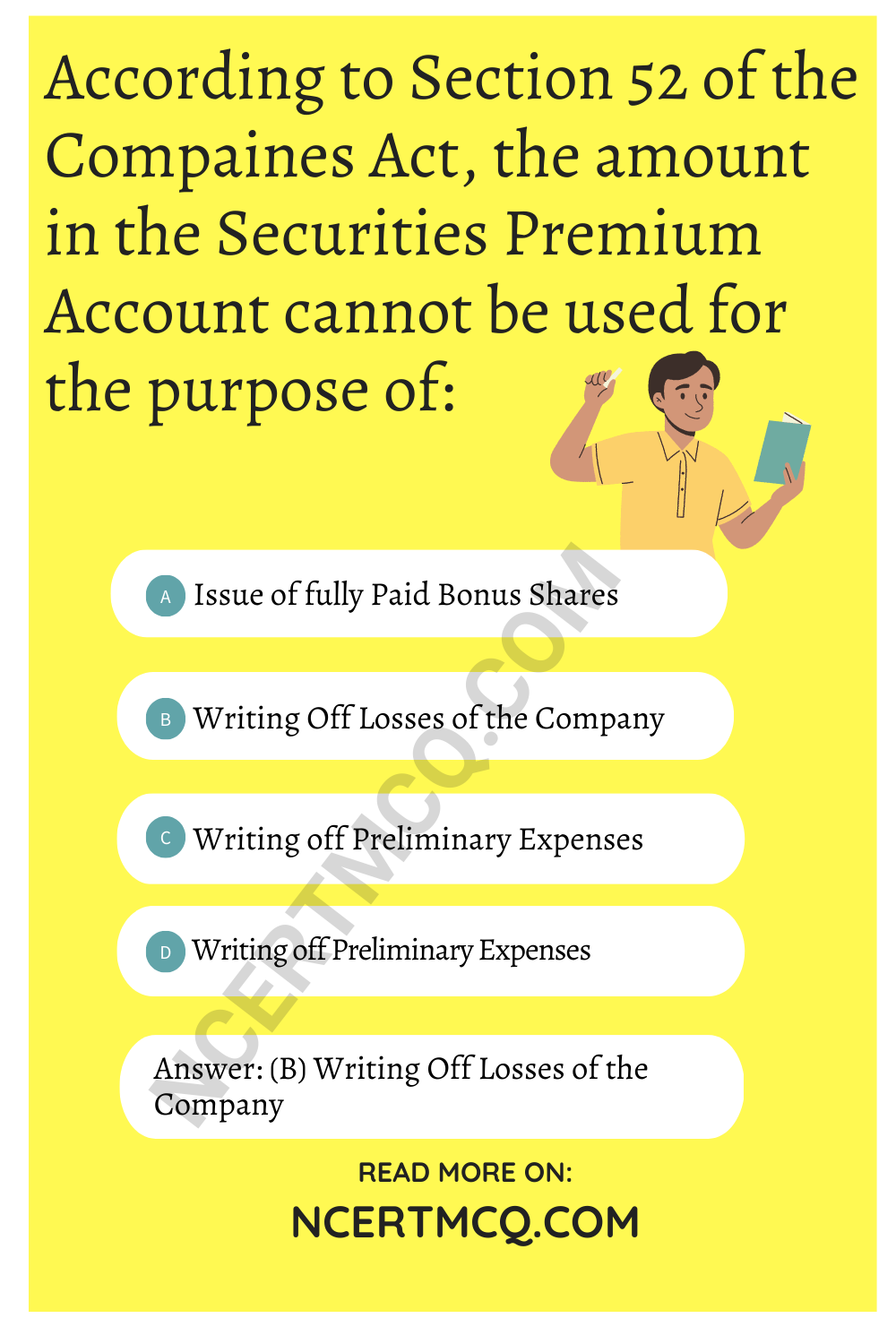

Question 50.

According to Section 52 of the Compaines Act, the amount in the Securities Premium Account cannot be used for the purpose of:

(a) Issue of fully Paid Bonus Shares

(b) Writing Off Losses of the Company

(c) Writing off Preliminary Expenses

(d) Writing Off Commission or Discount on Issue of Shares

Answer

Answer: (b) Writing Off Losses of the Company

Question 51.

10,000 equity shares of 10 Rs. each were issued to public at a premium of ₹ 2 per share payable on allotment.

Applications were received for ₹ 12,000 shares. Amount of securities premium account will be :

(a) ₹ 20,000

(b) ₹ 24,000

(c) ₹ 4,000

(d) ₹ 1,600

Answer

Answer: (a) ₹ 20,000

Question 52.

A Ltd. purchased a machinery for 1,80,000 Rs. for which it is paying by issue of shares of 100 Rs. each at 20% premium. How many shares will be issued as consideration. ?

(a) 2,500

(b) 2,000

(c) 1,500

(d) 3,000

Answer

Answer: (c) 1,500

Question 53.

Right Shares are issued to :

(a) Promoters for the Services

(b) Holders of Convertible Debentures

(c) Existing Shareholders

(d) All of the above

Answer

Answer: (c) Existing Shareholders

Question 54.

A company is registered with a share capital of ₹ 1,00,000 Rs. divided into ₹ 10,000 shares of ₹ 10 each. Of these shares 9,990 shares are held by Rajeev and 10 Shares are held by Sanjay. In the eye of law it is treated as:

(a) Partnership

(b) Private Company

(c) Public Compancy

(d) Government Company

Answer

Answer: (b) Private Company

Question 55.

Which of the following should be deducted from the called-up capital to find out paid-up capital:

(a) Calls-in-advance

(b) Calls-in-arrear

(c) Share forfeiture

(d) Discount on issue of shares

Answer

Answer: (b) Calls-in-arrear

We hope the given NCERT MCQ Questions for Class 12 Accountancy Chapter 6 Accounting for Share Capital with Answers Pdf free download will help you. If you have any queries regarding CBSE Class 12 Accountancy Accounting for Share Capital MCQs Multiple Choice Questions with Answers, drop a comment below and we will get back to you soon.

Class 12 Accountancy MCQ:

- Accounting for Not for Profit Organisation Class 12

- Accounting for Partnership: Basic Concepts Class 12

- Reconstitution of Partnership Firm: Admission of a Partner Class 12

- Reconstitution of Partnership Firm: Retirement / Death of a Partner Class 12

- Dissolution of a Partnership Firm Class 12

- Accounting for Share Capital Class 12

- Issue and Redemption of Debentures Class 12

- Financial Statements of a Company Class 12

- Analysis of Financial Statements Class 12

- Accounting Ratios Class 12

- Cash Flow Statement Class 12